From: Tomasz Tunguz <blog@tomtunguz.com>

Date: Fri, 28 Oct 2022 at 19:15

Subject: Grey Skies in Cloud Earnings

To: <martin@doversten.se>

Tomasz TunguzVenture Capitalist at Redpoint If you were forwarded this newsletter, and you'd like to receive it in the future, subscribe here. Grey Skies in Cloud Earnings

I’m watching public company earnings to identify early weaknesses in the software market. This week Microsoft, Google/ Alphabet, & Amazon reported their third quarter figures.

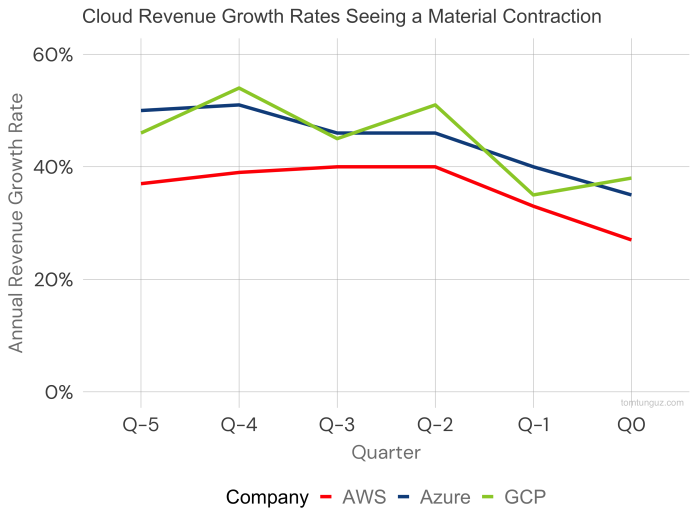

The meaningful decline in growth rates started four quarters ago is hard to ignore.

Customers spent $12b more this quarter - an astounding figure. At a 7x multiple of revenue, that is another $84b of market cap creation, in theory. But, the change in slope is meaningful, too. A year ago, these business units grew at 44% annually. The current recession is evident in the charts: growth rates have declined by 25% in six months’ time. The kink downwards in the red line at Q-2 shows a sudden deceleration in AWS’ growth rate. GCP is more volatile, likely driven by the volatility of bigger deals closing on a smaller revenue base. Meanwhile, Azure has declined in a more steady cadence. The data suggests a broader slowdown in software spending as these companies are indices of software buyers’ behavior. Public software multiples - 4.9x as of last week, not far from the decade low of 3.3x - should depress further given these results & forward guidance. Microsoft stock is down 10%; Amazon fell about 20%; Google about 12%. Lopping another 15% off multiples implies the median software company should trade at 4.2x forward revenues, a far cry from the 15x we observed not twelve months ago. If you didn’t enjoy the email you can unsubscribe here. 2969 Woodside Road, Woodside, CA 94062 |

Let’s put these figures into context. Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter.

Let’s put these figures into context. Infrastructure revenue growth averaged 33% this quarter, which is astounding considering we’re talking about businesses that sum to more than $50b of revenue per quarter.